Reverse mortgages have become an increasingly popular financial option for seniors looking to leverage their home equity for a more comfortable retirement. In Maine, a state known for its picturesque landscapes and vibrant communities, reverse mortgages are providing homeowners with new ways to fund their golden years. This article delves into the intricacies of reverse mortgages in Maine, offering insights into their benefits, requirements, and potential drawbacks.

As the baby boomer generation continues to age, many are seeking ways to make the most of their home's value without having to sell it. Reverse mortgages offer a unique solution, allowing homeowners aged 62 and older to convert part of their home equity into cash while retaining ownership. With Maine's distinct real estate market and economic conditions, understanding how reverse mortgages work in this state is crucial for making informed financial decisions.

Whether you're a homeowner considering a reverse mortgage or a family member seeking information for a loved one, this comprehensive guide will walk you through everything you need to know about reverse mortgage options in Maine. From eligibility criteria and application processes to potential risks and alternatives, we aim to provide you with the knowledge necessary to determine if a reverse mortgage is the right choice for you or your family.

Table of Contents

- What is a Reverse Mortgage?

- How Reverse Mortgages Work

- Eligibility Criteria in Maine

- Types of Reverse Mortgages

- Benefits of Reverse Mortgages

- Potential Risks and Considerations

- The Application Process

- Financial Planning with Reverse Mortgages

- Alternatives to Reverse Mortgages

- Reverse Mortgage Repayment

- Impact on Heirs and Estate

- Tax Implications

- Frequently Asked Questions

- Conclusion

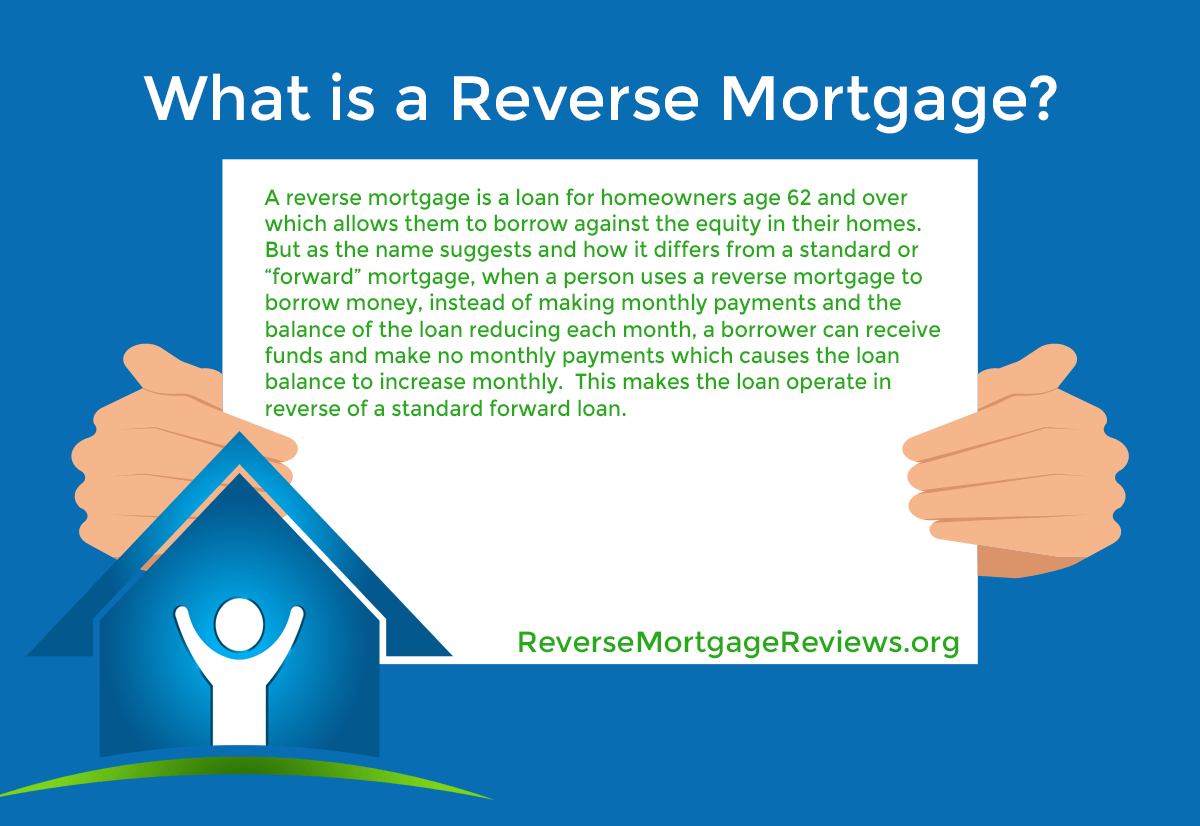

What is a Reverse Mortgage?

Reverse mortgages are a type of loan that allows homeowners aged 62 and above to convert part of their home equity into cash. Unlike traditional mortgages, which require monthly payments, reverse mortgages do not require repayment until the borrower moves out, sells the home, or passes away. This financial product can be particularly beneficial for retirees who have a significant portion of their wealth tied up in their home but need additional cash flow for living expenses.

How Reverse Mortgages Work

When a homeowner takes out a reverse mortgage, they receive payments based on the equity of their home. This can be in the form of a lump sum, monthly payments, a line of credit, or a combination of these options. The loan is secured by the home, meaning that the lender is repaid from the proceeds of the home's sale when the borrower no longer resides there. Importantly, homeowners retain ownership of their home during the life of the loan.

Eligibility Criteria in Maine

To qualify for a reverse mortgage in Maine, homeowners must meet certain criteria. They must be at least 62 years old, have significant equity in their home, and reside in the property as their primary residence. Additionally, the home must meet HUD standards, and the borrower must undergo a financial assessment to ensure they can afford ongoing property taxes and insurance.

Types of Reverse Mortgages

There are three main types of reverse mortgages available to homeowners in Maine: Home Equity Conversion Mortgages (HECMs), proprietary reverse mortgages, and single-purpose reverse mortgages. HECMs are federally insured and the most common type, while proprietary reverse mortgages are private loans that can offer larger loan amounts. Single-purpose reverse mortgages are typically offered by local government agencies or non-profits for specific purposes like home repairs.

Benefits of Reverse Mortgages

Reverse mortgages can provide several benefits to eligible Maine homeowners. These include supplemental income for retirees, the ability to stay in one's home while accessing its equity, and no monthly mortgage payments. Additionally, the funds received from a reverse mortgage are generally tax-free, providing a tax-advantaged way to supplement retirement income.

Potential Risks and Considerations

While reverse mortgages offer many benefits, there are also potential risks and considerations. These include the accumulation of interest over time, which can reduce the amount of equity left in the home for heirs. Additionally, borrowers are responsible for maintaining the property and paying property taxes and insurance. Failure to meet these obligations can lead to foreclosure.

The Application Process

The application process for a reverse mortgage in Maine involves several steps. Homeowners must complete a financial assessment, attend a counseling session with a HUD-approved counselor, and submit an application to a lender. Once approved, the homeowner can choose how they wish to receive their funds, whether as a lump sum, monthly payments, or a line of credit.

Financial Planning with Reverse Mortgages

Reverse mortgages can be an effective financial planning tool for seniors in Maine. They can provide additional cash flow for medical expenses, home modifications, or daily living costs. It is important for homeowners to work with financial advisors to understand how a reverse mortgage fits into their overall retirement plan and to explore other available options.

Alternatives to Reverse Mortgages

For those who may not qualify for a reverse mortgage or are exploring other options, there are alternatives to consider. These include home equity loans, home equity lines of credit (HELOCs), and downsizing to a smaller home. Each option has its own advantages and disadvantages, and should be carefully considered based on the homeowner's financial situation and goals.

Reverse Mortgage Repayment

Repayment of a reverse mortgage is typically due when the borrower moves out of the home, sells it, or passes away. At that time, the loan balance, which includes the principal and accumulated interest, must be repaid. This is usually done through the sale of the home. Borrowers or their heirs can also choose to repay the loan from other resources and retain ownership of the home.

Impact on Heirs and Estate

One of the primary concerns with reverse mortgages is their impact on heirs and the estate. Because the loan is repaid from the home's sale proceeds, it can reduce the amount of inheritance left to heirs. However, heirs are not personally liable for the loan if the home's value is less than the loan balance. They have the option to repay the loan and keep the home or sell it to satisfy the debt.

Tax Implications

Funds received from a reverse mortgage are generally considered loan proceeds and are not taxable income. However, borrowers should consult with a tax advisor to understand any potential tax implications, especially if they are using the funds for investment purposes. Additionally, interest on a reverse mortgage is not tax-deductible until it is paid, usually when the loan is repaid.

Frequently Asked Questions

What happens if the home value is less than the loan balance?

If the reverse mortgage balance exceeds the home's value, the borrower or their heirs are not responsible for the difference. Reverse mortgages are non-recourse loans, meaning the lender cannot seek repayment beyond the home's sale proceeds.

Can I lose my home with a reverse mortgage?

As long as you meet the loan obligations, such as paying property taxes, homeowner's insurance, and maintaining the home, you cannot lose your home due to the reverse mortgage.

How does a reverse mortgage affect Medicaid eligibility?

The proceeds from a reverse mortgage do not affect Medicaid eligibility, as they are considered loan advances. However, any funds retained as cash assets may impact Medicaid eligibility, so it's important to manage the funds carefully.

Can I use a reverse mortgage to purchase a new home?

Yes, a Home Equity Conversion Mortgage for Purchase (HECM for Purchase) allows seniors to buy a new primary residence using a reverse mortgage. This option can be beneficial for those looking to downsize or relocate.

What are the costs associated with a reverse mortgage?

Reverse mortgages typically include costs such as origination fees, closing costs, servicing fees, and mortgage insurance premiums. These costs can be rolled into the loan balance, reducing out-of-pocket expenses.

Is counseling required for a reverse mortgage?

Yes, counseling with a HUD-approved counselor is a mandatory step in the reverse mortgage process. It ensures borrowers understand the terms, costs, and implications of the loan before proceeding.

Conclusion

Reverse mortgages in Maine offer a valuable financial tool for seniors looking to access their home equity while remaining in their homes. By understanding the benefits, risks, and alternatives, homeowners can make informed decisions that align with their financial goals. As with any major financial decision, it's important to consult with financial advisors and consider all available options to ensure a secure and comfortable retirement.

For further information on reverse mortgages, you may refer to the Consumer Financial Protection Bureau's guide on reverse mortgages.

You Might Also Like

Our Generation Grill: A Modern Culinary ExperienceIn-Depth Profile Of Daniel Starks: Visionary Business Leader

Benefits And Importance Of The "109 89" Ratio In Financial Analysis

Vyvgart Hytrulo Cost: A Comprehensive Guide For Budgeting And Understanding

Romil Bahl: Innovator In The Tech Industry

Article Recommendations