In the world of real estate financing, the 3-2-1 buydown is a term that often surfaces, especially among homebuyers looking to ease their initial mortgage payments. This strategy offers a unique approach to managing mortgage costs, making it a popular choice among those who are financially cautious yet eager to step into homeownership. By reducing the interest rate for the first three years of the mortgage, a 3-2-1 buydown can provide significant financial relief in the early stages of a mortgage. This concept, while beneficial to some, requires a thorough understanding to ensure it aligns with one's long-term financial goals.

The 3-2-1 buydown option brings a blend of advantages and potential challenges. For homebuyers who anticipate an increase in income or a change in their financial situation within a few years, this option can be particularly advantageous. However, it's not without its pitfalls. Understanding the nuances of a 3-2-1 buydown can help buyers make informed decisions, potentially saving them thousands in interest payments, but also helping them avoid unexpected financial strain in the future. It is crucial for prospective buyers to carefully weigh the pros and cons, and consider their financial trajectory before committing to this type of mortgage.

As we delve into this article, we will explore the intricacies of the 3-2-1 buydown, examining each aspect with a critical eye. We aim to equip readers with the knowledge necessary to navigate the complexities of this financial tool. Through a detailed analysis of its workings, potential benefits, and drawbacks, this article serves as a comprehensive guide for understanding whether a 3-2-1 buydown is the right choice for individual financial circumstances. With the right insights, you can confidently decide if this mortgage strategy aligns with your homeownership goals and financial plans.

Table of Contents

- What is a 3-2-1 Buydown?

- How Does the 3-2-1 Buydown Work?

- Advantages of a 3-2-1 Buydown

- Potential Drawbacks of a 3-2-1 Buydown

- Who Benefits Most from a 3-2-1 Buydown?

- Comparing 3-2-1 Buydown to Other Mortgage Options

- 3-2-1 Buydown vs. ARM Loans

- Calculating Savings with a 3-2-1 Buydown

- Impact on Long-term Financial Planning

- Requirements and Eligibility for a 3-2-1 Buydown

- Negotiating a 3-2-1 Buydown with Lenders

- Real-life Examples and Case Studies

- Common Misconceptions About 3-2-1 Buydowns

- Frequently Asked Questions

- Conclusion

What is a 3-2-1 Buydown?

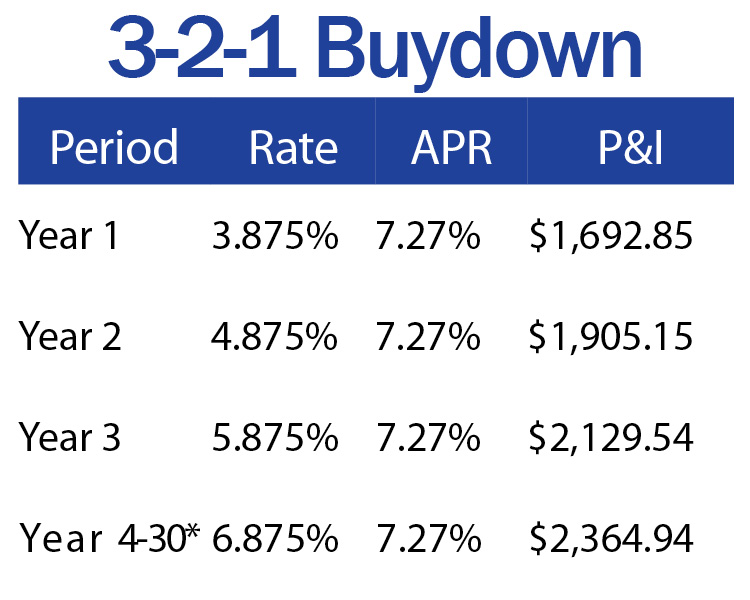

The 3-2-1 buydown is a mortgage financing technique that temporarily lowers the interest rate on a loan for the first three years. This strategy is designed to make monthly payments more affordable during the initial years of homeownership. In a 3-2-1 buydown, the interest rate is reduced by 3% in the first year, 2% in the second year, and 1% in the third year, ultimately reaching the original rate in the fourth year and remaining constant for the remainder of the loan term.

This type of buydown can be an appealing option for first-time homebuyers or those who expect their income to increase over time. By offering a lower monthly payment initially, it can provide financial breathing room during the early years of the mortgage, allowing homeowners to adjust to their new financial obligations gradually.

However, the 3-2-1 buydown is not a free service. The cost of the reduced interest rates is typically covered by an upfront fee paid by the buyer or sometimes the seller or builder as an incentive to close the sale. This fee is calculated based on the difference between the original interest rate and the reduced rates over the three-year period. Understanding the exact cost of the buydown and how it's structured is crucial for making an informed decision.

How Does the 3-2-1 Buydown Work?

The mechanics of a 3-2-1 buydown are relatively straightforward, but they require careful attention to detail. The process begins with the lender agreeing to a lower interest rate for the initial years of the mortgage. This is made possible by a buydown fund, which is essentially a subsidy that covers the difference between the reduced and original interest rates during the buydown period.

In practical terms, if you start with a 6% interest rate on a 30-year fixed mortgage, the rate would be 3% in the first year, 4% in the second year, and 5% in the third year. From the fourth year onward, the interest rate returns to the original 6% and remains constant for the remainder of the loan term. The savings in interest payments from the reduced rates are what make the buydown attractive, especially for buyers who need lower payments upfront.

The cost of the buydown is typically negotiated between the buyer, seller, and lender. It can be financed in various ways, such as being paid by the seller as a closing cost incentive, by the buyer as part of their mortgage closing costs, or rolled into the loan amount. Each method has its implications, affecting the overall cost of the mortgage and the buyer's financial position.

Advantages of a 3-2-1 Buydown

The 3-2-1 buydown offers several compelling benefits, making it an attractive option for many homebuyers. One of the most significant advantages is the immediate reduction in monthly mortgage payments. This can be particularly beneficial for buyers who may not yet be earning their full potential income or those who anticipate their financial situation improving in the near future.

Another advantage is the flexibility it provides. By lowering monthly payments during the initial years, homeowners have the opportunity to allocate funds toward other financial goals, such as building an emergency fund, paying off high-interest debt, or investing in home improvements that can increase the property's value.

Furthermore, a 3-2-1 buydown can make homeownership more accessible for first-time buyers who might otherwise struggle to meet higher monthly payments. The initial cost savings can ease the transition into homeownership, making it a less daunting financial commitment.

Potential Drawbacks of a 3-2-1 Buydown

While the 3-2-1 buydown offers several benefits, it also comes with its share of potential drawbacks. One of the primary concerns is the upfront cost. The buydown requires a lump-sum payment to cover the interest rate reduction, which can be a significant expense. Buyers need to carefully evaluate whether the initial savings justify this cost.

Additionally, if the buyer's financial situation does not improve as anticipated, they may find themselves struggling to meet the higher payments once the buydown period ends. This can lead to financial stress and, in some cases, the risk of default.

Another potential drawback is that not all lenders offer 3-2-1 buydown options, and those that do may impose specific conditions or restrictions. Buyers must ensure they fully understand the terms and conditions of the buydown agreement before proceeding.

Who Benefits Most from a 3-2-1 Buydown?

The 3-2-1 buydown is best suited for homebuyers who anticipate an increase in their income or a significant change in their financial situation within a few years. This includes young professionals in growing careers, individuals expecting a substantial salary increase, or buyers planning to refinance their mortgage before the buydown period ends.

It can also be beneficial for buyers who have a clear plan to increase their financial stability, such as reducing debt or building up savings. Additionally, first-time homebuyers who want to ease into the financial responsibilities of homeownership may find the 3-2-1 buydown advantageous.

Ultimately, the suitability of a 3-2-1 buydown depends on the buyer's financial goals, risk tolerance, and long-term plans. Buyers should carefully consider their unique circumstances and consult with a financial advisor or mortgage professional to determine if this option aligns with their needs.

Comparing 3-2-1 Buydown to Other Mortgage Options

When considering a 3-2-1 buydown, it's essential to compare it with other mortgage options to determine which best suits your needs. One common alternative is a fixed-rate mortgage, which offers stability and predictability in monthly payments. Unlike a 3-2-1 buydown, a fixed-rate mortgage does not involve upfront costs for lowering the interest rate, making it a straightforward choice for those who prefer consistency.

Adjustable-rate mortgages (ARMs) are another option to consider. While ARMs often start with lower interest rates, they can fluctuate over time, introducing an element of uncertainty. Buyers who are comfortable with potential changes in their monthly payments might find ARMs appealing, but they should weigh this against the stability of a 3-2-1 buydown.

Ultimately, the best mortgage option depends on individual financial goals, risk tolerance, and long-term plans. Buyers should carefully evaluate the pros and cons of each option and consider consulting with a mortgage professional to make an informed decision.

3-2-1 Buydown vs. ARM Loans

The choice between a 3-2-1 buydown and an adjustable-rate mortgage (ARM) depends on various factors, including financial stability, risk tolerance, and future plans. While both options offer initial lower payments, they differ significantly in their structure and long-term implications.

With a 3-2-1 buydown, the interest rate is temporarily reduced and then returns to a fixed rate for the remainder of the mortgage term. This provides predictability and stability once the buydown period ends. In contrast, ARMs have variable interest rates that can fluctuate based on market conditions, leading to potential changes in monthly payments over time.

Buyers who prefer predictability and can manage the upfront cost of a buydown might lean towards a 3-2-1 buydown, while those who are comfortable with potential rate changes and seek lower initial payments without an upfront cost might consider an ARM.

Calculating Savings with a 3-2-1 Buydown

One of the key aspects of evaluating a 3-2-1 buydown is understanding the potential savings it offers. To calculate the savings, buyers need to compare the total interest paid with the buydown against the interest paid with a standard loan at the original rate.

Consider a $300,000 mortgage with an original interest rate of 6%. With a 3-2-1 buydown, the first year's rate would be 3%, the second year's 4%, and the third year's 5%. Buyers can calculate the monthly payments for each year and the total interest paid over the buydown period, then compare it to the interest paid without the buydown.

While the buydown offers upfront savings, buyers must also consider the cost of the buydown itself. By weighing these factors, buyers can determine if the 3-2-1 buydown provides meaningful financial benefits in their specific situation.

Impact on Long-term Financial Planning

The 3-2-1 buydown can have a significant impact on long-term financial planning. By reducing monthly payments in the early years, buyers may have more flexibility to allocate funds towards other financial goals, such as savings, investments, or debt reduction.

However, buyers must also consider the implications of higher payments once the buydown period ends. Ensuring that their financial situation can accommodate these payments is crucial to avoid financial strain.

Buyers should also evaluate how the buydown fits into their broader financial goals, such as retirement planning or purchasing additional properties. By taking a holistic approach to their financial planning, buyers can determine if a 3-2-1 buydown aligns with their long-term objectives.

Requirements and Eligibility for a 3-2-1 Buydown

To qualify for a 3-2-1 buydown, buyers typically need to meet specific eligibility criteria set by lenders. These requirements may include a minimum credit score, a stable income, and sufficient funds to cover the cost of the buydown.

Lenders may also impose additional conditions, such as requiring a certain down payment amount or verifying the buyer's ability to afford the higher payments once the buydown period ends. Buyers should work closely with their lender to understand the specific requirements and ensure they meet the eligibility criteria.

Additionally, buyers should be prepared to provide documentation supporting their financial situation, such as income statements, tax returns, and bank statements. By meeting these requirements, buyers can increase their chances of securing a 3-2-1 buydown.

Negotiating a 3-2-1 Buydown with Lenders

Negotiating a 3-2-1 buydown with lenders involves understanding the terms and costs associated with the buydown and effectively communicating with the lender to reach an agreement.

Buyers should start by researching different lenders and their buydown options, comparing the terms and costs offered by each. By gathering this information, buyers can gain a better understanding of the market and identify potential opportunities for negotiation.

When negotiating, buyers should be prepared to discuss their financial situation, long-term goals, and how the 3-2-1 buydown aligns with those objectives. By presenting a clear and compelling case, buyers can increase their chances of securing favorable terms.

Additionally, buyers may consider seeking assistance from a mortgage broker or financial advisor, who can provide valuable insights and guidance throughout the negotiation process.

Real-life Examples and Case Studies

Examining real-life examples and case studies can provide valuable insights into the potential benefits and drawbacks of a 3-2-1 buydown. By analyzing different scenarios, buyers can gain a better understanding of how the buydown may impact their financial situation and decision-making process.

For example, consider a young couple who recently purchased their first home. By opting for a 3-2-1 buydown, they were able to reduce their initial monthly payments, allowing them to allocate funds towards other financial goals, such as building an emergency fund and saving for future home improvements.

Alternatively, consider a buyer who anticipated an income increase but faced unexpected financial challenges. As a result, they struggled to meet the higher payments once the buydown period ended, leading to financial stress and the need to reevaluate their financial strategy.

By exploring these examples, buyers can gain valuable insights into the potential outcomes of a 3-2-1 buydown and make more informed decisions based on their unique circumstances.

Common Misconceptions About 3-2-1 Buydowns

There are several common misconceptions about 3-2-1 buydowns that can lead to confusion and misunderstandings among buyers. One such misconception is that the buydown is a free or costless option. In reality, the buydown requires an upfront payment to cover the reduced interest rates, which can be a significant expense for buyers.

Another misconception is that the buydown automatically results in long-term savings. While the buydown offers initial savings, buyers must consider the overall cost and potential impact on their financial situation once the buydown period ends.

Finally, some buyers may mistakenly believe that all lenders offer 3-2-1 buydown options. In reality, not all lenders provide this option, and those that do may impose specific conditions or restrictions.

By addressing these misconceptions, buyers can gain a clearer understanding of the 3-2-1 buydown and make more informed decisions about their mortgage options.

Frequently Asked Questions

- What is a 3-2-1 buydown?

A 3-2-1 buydown is a mortgage financing technique that temporarily reduces the interest rate for the first three years of a home loan, making initial payments more affordable. - How does a 3-2-1 buydown work?

In a 3-2-1 buydown, the interest rate is reduced by 3% in the first year, 2% in the second year, and 1% in the third year, before returning to the original rate in the fourth year. - Who can benefit from a 3-2-1 buydown?

Buyers anticipating an increase in income or a change in their financial situation within a few years may benefit from a 3-2-1 buydown, as it provides lower initial payments. - What are the potential drawbacks of a 3-2-1 buydown?

The upfront cost, the risk of financial strain once the buydown period ends, and the limited availability among lenders are potential drawbacks of a 3-2-1 buydown. - How do I qualify for a 3-2-1 buydown?

Qualifying for a 3-2-1 buydown typically involves meeting specific lender requirements, such as a minimum credit score, stable income, and sufficient funds to cover the buydown cost. - Can I negotiate a 3-2-1 buydown with my lender?

Yes, buyers can negotiate the terms and costs of a 3-2-1 buydown with their lender, potentially securing more favorable conditions.

Conclusion

The 3-2-1 buydown offers a unique approach to mortgage financing, providing lower initial payments and potential financial relief for homebuyers. However, it is not without its challenges, including upfront costs and the need for careful financial planning. By understanding the intricacies of a 3-2-1 buydown and considering individual financial goals, buyers can make informed decisions that align with their needs and long-term objectives.

Ultimately, the suitability of a 3-2-1 buydown depends on various factors, including financial stability, risk tolerance, and future plans. Buyers should carefully evaluate their options, consult with financial professionals, and consider real-life examples to determine if this mortgage strategy is the right fit for their unique circumstances.

For further information on mortgage options and financial planning, consider visiting Consumer Financial Protection Bureau for additional resources and guidance.

You Might Also Like

Michael Schmertzler: A Visionary Leader In Finance And PhilanthropyEmily D. Baker Net Worth: A Deep Dive Into Her Career And Success

PMT Ex-Dividend Date: Crucial Insights For Investors

Convenient Christmas Tree Delivery Services In DC

Insights Into Dave Moellenhoff's Impact On Technology And Beyond

Article Recommendations