In the world of mutual funds, investors are often faced with the decision between choosing a direct mutual fund or a regular mutual fund. This choice can significantly impact the overall returns on investment. Understanding the differences between these two options is crucial for making informed investment decisions that align with your financial goals. With the evolution of technology and increased financial literacy, investors now have access to more information than ever before, empowering them to make smarter choices.

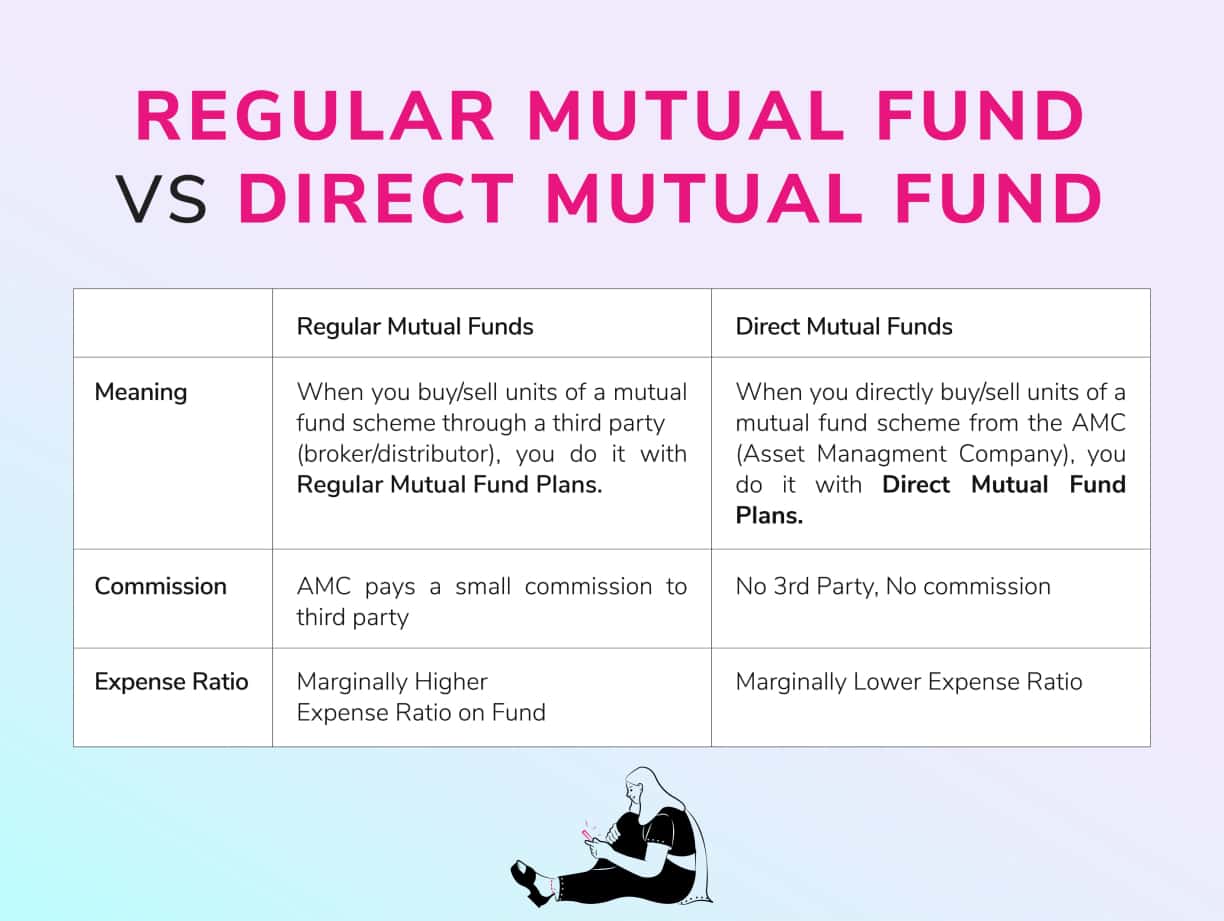

Direct mutual funds and regular mutual funds are two distinct paths investors can take when allocating their resources in mutual funds. While they both serve the same fundamental purpose of helping investors build wealth over time, the difference lies in the cost structure and the way these funds are managed. Direct mutual funds are purchased directly from the fund house, eliminating the need for intermediaries, whereas regular mutual funds involve a third party, typically a broker or advisor, who assists in the investment process and charges a commission for their services.

With the growing popularity of mutual funds as a preferred investment vehicle, the debate over direct mutual fund vs regular mutual fund has gained momentum. Investors are increasingly seeking clarity on which option offers better returns, lower costs, and aligns with their risk appetite. Navigating through the advantages and potential pitfalls of each type of mutual fund can help investors make the right choice for their unique financial situation. This article delves into the nuances of both direct and regular mutual funds, providing a comprehensive guide to help investors make informed decisions.

Table of Contents

- What Are Mutual Funds?

- Understanding Direct Mutual Funds

- Understanding Regular Mutual Funds

- Cost Structure and Fees

- Performance and Returns

- Ease of Access and Convenience

- Role of Financial Advisors

- Investment Goals and Risk Appetite

- Tax Implications

- Making the Right Choice

- Common Myths and Misconceptions

- Impact of Technology

- Case Studies and Real-World Examples

- Frequently Asked Questions

- Conclusion

What Are Mutual Funds?

Mutual funds are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. Managed by professional fund managers, mutual funds offer investors access to a broad range of asset classes and investment strategies. The primary advantage of mutual funds is the ability to achieve diversification, reducing the risk associated with investing in individual securities.

With mutual funds, investors can participate in a wide array of investment opportunities without needing to have large sums of money. This accessibility makes mutual funds an attractive option for both beginner and seasoned investors. Mutual funds are categorized into various types, such as equity funds, debt funds, hybrid funds, and more, each serving different investment objectives and risk profiles.

The structure of a mutual fund involves the creation of units, which investors can purchase based on the net asset value (NAV) of the fund. The NAV is calculated by dividing the total market value of the fund's assets by the number of outstanding units. Investors earn returns through dividends, interest, and capital gains generated by the underlying assets in the fund's portfolio.

Understanding Direct Mutual Funds

Direct mutual funds are a relatively recent innovation in the mutual fund industry, designed to provide investors with a cost-effective alternative to traditional regular mutual funds. With direct mutual funds, investors can purchase units directly from the fund house, bypassing intermediaries such as brokers or financial advisors. This direct approach results in lower expense ratios, as there are no commission fees to pay to intermediaries.

The introduction of direct mutual funds was aimed at empowering investors by enabling them to take control of their investment decisions. With the proliferation of online platforms and digital tools, investors can easily access information about various mutual fund schemes, compare their performance, and invest in direct mutual funds without the need for third-party assistance.

Investors who choose direct mutual funds benefit from the potential for higher returns, as the cost savings from lower expense ratios are directly passed on to the investors. However, investing in direct mutual funds requires a certain level of financial literacy and comfort with making independent investment decisions, as the absence of intermediaries means investors must conduct their own research and analysis.

Understanding Regular Mutual Funds

Regular mutual funds, on the other hand, involve the use of intermediaries such as brokers, financial advisors, or distributors who facilitate the investment process on behalf of investors. In exchange for their services, these intermediaries charge a commission, which is included in the expense ratio of the mutual fund. As a result, regular mutual funds typically have higher expense ratios compared to direct mutual funds.

The role of intermediaries in regular mutual funds is to assist investors with selecting suitable mutual fund schemes, providing investment advice, and managing the administrative aspects of the investment process. This service can be particularly valuable for investors who may not have the time, expertise, or inclination to manage their investments independently.

Despite the higher costs associated with regular mutual funds, many investors prefer this option due to the personalized guidance and support provided by financial advisors. For individuals who value professional advice and prefer a hands-off approach to investing, regular mutual funds offer the convenience of having a trusted advisor manage their investment portfolio.

Cost Structure and Fees

The cost structure of mutual funds is a critical factor that influences an investor's decision between direct mutual funds and regular mutual funds. The primary components of mutual fund costs include the expense ratio, exit load, and transaction fees. The expense ratio represents the annual fees charged by the fund house to cover the costs of managing the fund, expressed as a percentage of the fund's average assets under management (AUM).

Direct mutual funds have lower expense ratios compared to regular mutual funds, as they do not incur commission fees paid to intermediaries. This cost advantage translates into higher net returns for investors over the long term, making direct mutual funds an attractive option for cost-conscious investors.

Regular mutual funds, while having higher expense ratios, offer the benefit of professional advice and support from financial advisors. For some investors, the value of expert guidance and the convenience of having a financial advisor manage their investments outweigh the additional costs associated with regular mutual funds.

Additionally, both direct and regular mutual funds may charge an exit load, which is a fee imposed on investors who redeem their units before a specified period. Transaction fees, such as account opening charges and transaction processing fees, may also apply, depending on the fund house and the investment platform used.

Performance and Returns

The performance and returns of mutual funds are influenced by various factors, including the fund manager's expertise, the investment strategy, and prevailing market conditions. Both direct and regular mutual funds invest in the same underlying assets, and their performance is measured by the same benchmarks.

However, the difference in expense ratios between direct and regular mutual funds can impact the net returns realized by investors. Direct mutual funds, with their lower expense ratios, typically offer higher net returns compared to their regular counterparts. Over the long term, the cost savings from investing in direct mutual funds can result in significant differences in wealth accumulation.

It's important to note that past performance is not indicative of future results, and investors should consider other factors, such as investment objectives, risk tolerance, and time horizon, when evaluating mutual fund performance. Investors should also conduct thorough research and due diligence when selecting mutual fund schemes, regardless of whether they choose direct or regular mutual funds.

Ease of Access and Convenience

In terms of ease of access and convenience, direct mutual funds and regular mutual funds offer different experiences to investors. Direct mutual funds are accessible through online platforms and mobile applications provided by fund houses or third-party investment platforms. This digital approach allows investors to easily compare mutual fund schemes, monitor their portfolio, and execute transactions from the comfort of their homes.

Regular mutual funds, on the other hand, offer the convenience of having a financial advisor manage the investment process. Advisors facilitate the investment process, providing personalized recommendations and handling the administrative tasks associated with investing in mutual funds. This service is particularly beneficial for investors who prefer a more hands-off approach to managing their portfolios.

Ultimately, the choice between direct and regular mutual funds in terms of access and convenience depends on an investor's preferences and comfort level with using digital tools and platforms for investment purposes. While direct mutual funds offer greater control and lower costs, regular mutual funds provide the advantage of professional guidance and support.

Role of Financial Advisors

Financial advisors play a significant role in the investment process, particularly for investors who choose regular mutual funds. Advisors provide valuable insights and recommendations based on an investor's financial goals, risk tolerance, and investment horizon. They assist in constructing a diversified portfolio that aligns with the investor's objectives and manage the ongoing monitoring and rebalancing of the portfolio.

For investors who lack the time or expertise to manage their investments independently, financial advisors offer a level of comfort and confidence in the investment process. Advisors also help investors navigate complex financial products, tax implications, and market trends, ensuring that investment decisions are well-informed and aligned with personal financial goals.

While the services of financial advisors come at a cost, many investors find the value of expert guidance and personalized support outweighs the additional fees associated with regular mutual funds. Ultimately, the decision to engage a financial advisor should be based on individual preferences, financial literacy, and the complexity of the investor's financial situation.

Investment Goals and Risk Appetite

Investment goals and risk appetite are crucial factors that influence an investor's choice between direct mutual funds and regular mutual funds. Different investors have varying financial objectives, such as wealth accumulation, retirement planning, or funding specific life events. These goals determine the appropriate asset allocation and investment strategy.

Investors with a higher risk tolerance may prefer equity-oriented mutual funds, while those with a lower risk appetite may opt for debt or balanced funds. The choice between direct and regular mutual funds also depends on the investor's willingness to take on the responsibility of managing their portfolio.

Direct mutual funds are suitable for investors who are confident in their ability to conduct independent research and make informed investment decisions. These investors prioritize cost savings and are comfortable using digital platforms to manage their investments.

In contrast, investors who value expert guidance and prefer a hands-off approach may opt for regular mutual funds. The involvement of a financial advisor can provide peace of mind and ensure that investment decisions align with the investor's goals and risk profile.

Tax Implications

Tax implications are an essential consideration for investors when selecting mutual funds. Both direct and regular mutual funds are subject to the same tax treatment, which depends on the type of fund and the investment horizon.

Equity mutual funds, for example, are subject to short-term capital gains tax if units are redeemed within one year, and long-term capital gains tax if held for more than one year. Debt mutual funds have different tax implications, with indexation benefits available for long-term capital gains.

Investors should consider the tax efficiency of their investment choices and factor in potential tax liabilities when evaluating the overall returns from mutual funds. Working with a financial advisor or tax professional can help investors navigate the complexities of tax regulations and optimize their investment strategy for tax efficiency.

Making the Right Choice

The decision between direct mutual funds and regular mutual funds ultimately depends on individual preferences, financial goals, and investment experience. Investors should weigh the pros and cons of each option, considering factors such as cost, convenience, access to professional guidance, and personal investment objectives.

For cost-conscious investors with the confidence and capability to manage their investments independently, direct mutual funds offer the advantage of lower expense ratios and the potential for higher returns. On the other hand, investors who value personalized advice and the convenience of having a financial advisor manage their portfolio may find regular mutual funds to be a more suitable choice.

Ultimately, the right choice will vary for each investor, and it's essential to conduct thorough research and consider all relevant factors before making an investment decision. Whether opting for direct or regular mutual funds, investors should prioritize aligning their investment strategy with their financial goals and risk appetite.

Common Myths and Misconceptions

There are several common myths and misconceptions surrounding direct and regular mutual funds that can influence investors' perceptions and decisions. One myth is that direct mutual funds are inherently riskier than regular mutual funds. In reality, both types of mutual funds invest in the same underlying assets, and the risk profile depends on the specific fund and its investment strategy.

Another misconception is that regular mutual funds always offer better returns due to professional management. While financial advisors provide valuable guidance, the higher expense ratios of regular mutual funds can impact net returns. Direct mutual funds, with their lower costs, may offer higher returns over the long term, assuming similar performance.

It's also important to note that choosing direct mutual funds does not mean investors are entirely on their own. Many fund houses and online platforms offer educational resources, tools, and support to help investors make informed decisions. Understanding these myths and misconceptions is crucial for making well-informed investment choices.

Impact of Technology

Technology has played a transformative role in the mutual fund industry, making investing more accessible and convenient for investors. The rise of digital platforms and mobile applications has empowered investors to explore and invest in mutual funds with ease, particularly direct mutual funds.

These platforms provide investors with real-time access to information, performance data, and analytical tools, enabling them to make informed investment decisions. The ability to compare mutual fund schemes, track portfolio performance, and execute transactions online has democratized the investment process, allowing investors to take control of their financial future.

For regular mutual funds, technology has enhanced the efficiency of financial advisors, enabling them to offer more personalized and data-driven advice to clients. Advisors can leverage technology to streamline administrative tasks, monitor market trends, and tailor investment recommendations based on individual client needs.

Case Studies and Real-World Examples

Examining case studies and real-world examples can provide valuable insights into the experiences of investors who have chosen direct or regular mutual funds. These examples illustrate the potential outcomes and considerations that investors may encounter when making their investment decisions.

One example involves an investor who switched from regular mutual funds to direct mutual funds after realizing the impact of expense ratios on their portfolio's performance. Over time, the cost savings from lower expense ratios contributed to higher net returns, significantly increasing the investor's wealth accumulation.

Another example highlights an investor who preferred the guidance of a financial advisor and remained invested in regular mutual funds. The advisor's expertise helped the investor navigate market volatility, make timely investment decisions, and achieve their financial goals, despite the higher cost of regular mutual funds.

These case studies underscore the importance of aligning investment choices with individual preferences, financial goals, and risk tolerance. Understanding the experiences of other investors can help individuals make more informed decisions when evaluating direct mutual fund vs regular mutual fund options.

Frequently Asked Questions

1. What is the main difference between direct and regular mutual funds?

The main difference lies in the cost structure. Direct mutual funds are purchased directly from the fund house, resulting in lower expense ratios due to the absence of intermediary commissions. Regular mutual funds involve intermediaries, incurring higher expense ratios due to commission fees.

2. Can I switch from regular mutual funds to direct mutual funds?

Yes, investors can switch from regular to direct mutual funds. However, this may involve redeeming units in the regular fund and purchasing units in the direct fund, potentially triggering exit loads and tax implications.

3. Are direct mutual funds riskier than regular mutual funds?

No, both direct and regular mutual funds invest in the same underlying assets, and the risk profile depends on the specific fund and its investment strategy. The choice between the two does not inherently affect risk.

4. Do direct mutual funds offer better returns than regular mutual funds?

Direct mutual funds typically offer higher net returns due to lower expense ratios. However, the actual returns depend on the performance of the underlying assets and the fund manager's expertise.

5. Do I need a financial advisor to invest in mutual funds?

No, investors can choose to invest in direct mutual funds without a financial advisor. However, those who prefer professional guidance and support may benefit from working with a financial advisor when investing in regular mutual funds.

6. How do I decide between direct and regular mutual funds?

Consider factors such as cost, convenience, access to professional guidance, investment goals, and risk tolerance. Conduct thorough research and evaluate which option aligns best with your financial objectives and preferences.

Conclusion

Choosing between direct mutual fund vs regular mutual fund is a crucial decision that can significantly impact an investor's financial journey. Each option offers distinct advantages and considerations, and the right choice depends on individual preferences, financial goals, and investment experience. Direct mutual funds provide cost savings and potential for higher returns, while regular mutual funds offer the benefit of personalized guidance and professional support. By understanding the nuances of each option, investors can make informed decisions that align with their financial objectives and risk appetite, ultimately paving the way for a successful investment journey.

You Might Also Like

Alluring Sour Garlic Mints Strain: A Comprehensive GuideEthena Crypto Price Prediction: A Visionary Outlook For Investors

Insights Into The Life And Achievements Of Hiller Michael: A Remarkable Journey

Insights On Mario Ferruzzi: Visionary In Nutrition Science

Ignite Funding Reviews: Your Path To Smart Investments

Article Recommendations

- Tia Alannah Borso Latest News Updates

- Hear The Heartpounding Chaparro Chuacheneger Singing

- Sandy Sabara