When it comes to investing in index funds, two names often rise to the top: Schwab and Vanguard. These financial giants have carved out significant niches in the world of low-cost, passive investing, attracting millions of investors worldwide. Understanding the nuances of Schwab index funds vs Vanguard is crucial for anyone looking to make informed investment decisions. Each company offers a unique set of advantages and potential drawbacks, making the choice between them a significant one for investors seeking to maximize their returns while minimizing costs.

Index funds have gained popularity due to their ability to offer broad market exposure, low operating expenses, and a passive investment strategy that has historically outperformed many actively managed funds. Schwab and Vanguard are both pioneers in this field, offering a wide range of index funds tailored to meet diverse investment goals and risk appetites. As these companies compete for investor dollars, they continue to innovate and refine their offerings, providing investors with more choices and better tools to manage their portfolios.

In this article, we will delve into a comprehensive comparison between Schwab index funds and Vanguard, examining their histories, fund offerings, fees, performance, and more. By the end of this analysis, you will have a clearer understanding of which provider might be better suited to your investment needs and how to leverage their respective strengths to achieve your financial objectives. So, whether you're a seasoned investor or just starting out, read on to discover how Schwab and Vanguard measure up in the world of index funds.

Table of Contents

- History and Backgrounds

- Investment Philosophies

- Range of Index Funds

- Fee Structures

- Performance Analysis

- Customer Service

- Online Platforms and Tools

- Social Responsibility and Ethics

- Tax Efficiency

- Investment Minimums

- Reputation and Credibility

- Pros and Cons

- FAQs

- Conclusion

History and Backgrounds

The history of Schwab and Vanguard is rich with innovation and a dedication to investor-centric solutions. Founded in 1971 by Charles Schwab, the Charles Schwab Corporation has grown to become one of the largest financial services firms in the United States. Schwab's mission has always been to make investing accessible to the average person, pioneering the discount brokerage model that has since become industry standard.

Vanguard, on the other hand, was founded by John C. Bogle in 1975. Bogle is often credited with creating the first index fund available to retail investors, the Vanguard 500 Index Fund. This revolutionary idea was based on the belief that keeping costs low and investing in a broad market index would yield better returns for investors over the long term. Today, Vanguard remains a leader in passive investing, managing over $7 trillion in global assets.

Investment Philosophies

Both Schwab and Vanguard adhere to a philosophy of low-cost investing, but their approaches vary slightly. Schwab emphasizes investor choice, offering a wide range of index funds as well as actively managed funds and ETFs. They focus on making investing as straightforward and affordable as possible, often reducing fees to remain competitive.

Vanguard, meanwhile, is renowned for its investor-owned structure, meaning its funds are owned by the investors themselves. This unique setup aligns Vanguard's interests with those of its investors, allowing for lower costs and a focus on long-term returns. Vanguard champions the idea that minimizing costs and investing for the long-term are the keys to successful investing.

Range of Index Funds

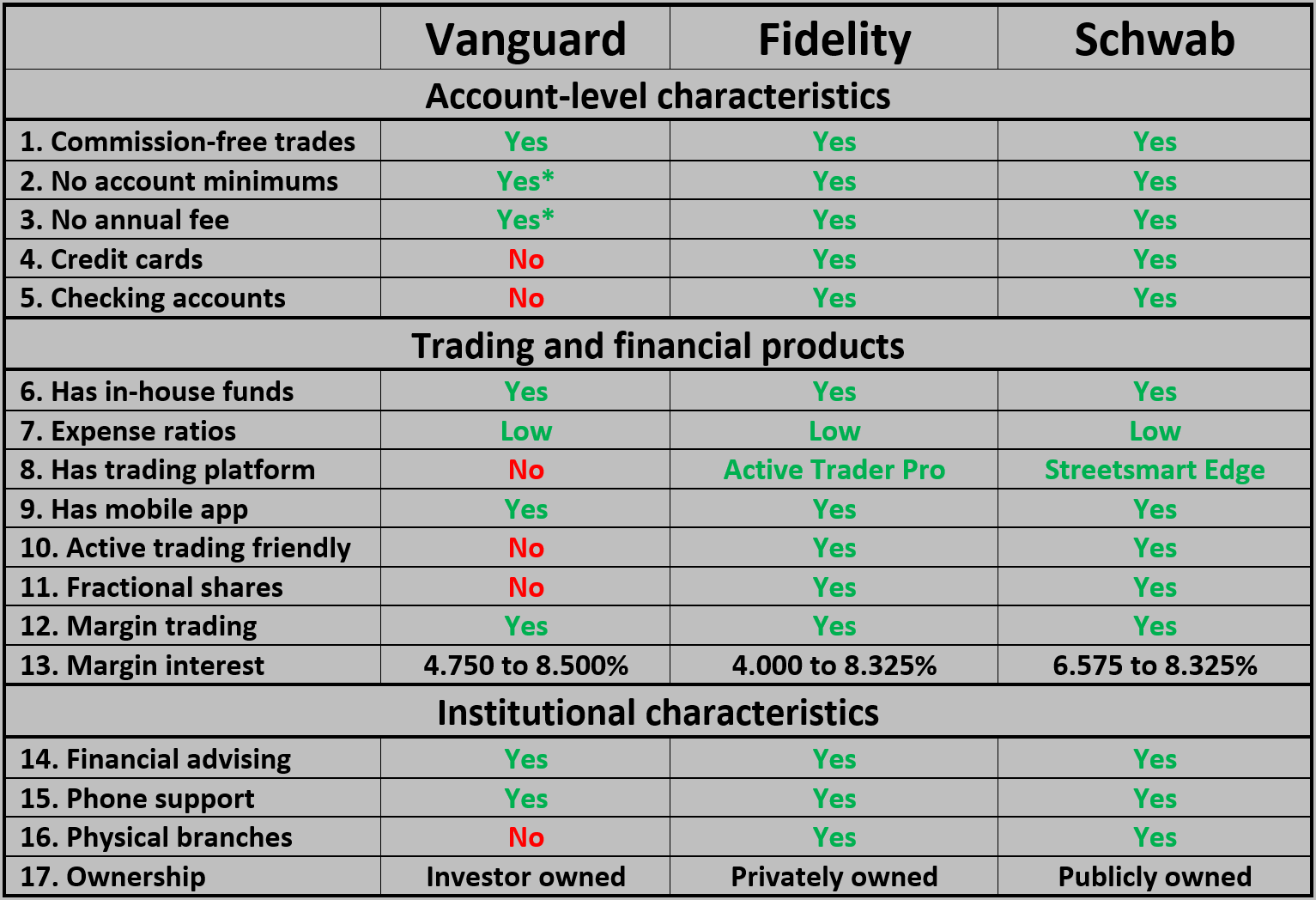

When comparing Schwab index funds vs Vanguard, it's essential to consider the breadth and variety of index funds each offers. Schwab provides a robust selection of index funds that cover U.S. stocks, international stocks, bonds, and more. They continue to expand their offerings to provide investors with options that suit different risk tolerances and investment goals.

Vanguard, however, is often seen as the benchmark for index fund offerings. With a comprehensive suite of funds covering nearly every conceivable asset class and sector, Vanguard provides investors with the tools to build a diversified portfolio tailored to their specific needs. Their funds are known for their low expense ratios, which can make a significant difference in long-term investment returns.

Fee Structures

Fees are a critical consideration when investing in index funds, and both Schwab and Vanguard are committed to keeping costs low. Schwab offers some of the lowest expense ratios in the industry, often setting the bar for competitor pricing. Their index funds typically come with no transaction fees, making them an attractive option for cost-conscious investors.

Vanguard is equally competitive when it comes to fees, with many of their index funds boasting expense ratios lower than the industry average. Their unique ownership structure allows them to pass savings directly to investors, enabling them to maintain low costs while still providing robust investment options.

Performance Analysis

Performance is a crucial factor for investors evaluating Schwab index funds vs Vanguard. Historically, both companies have delivered strong returns across their index fund offerings. However, differences in performance can arise based on the specific index tracked, fund management strategies, and market conditions.

Investors should consider performance in conjunction with other factors like fees, risk, and investment goals. Comparing historical performance data and examining the consistency of returns can help investors make informed decisions regarding which provider aligns best with their investment strategy.

Customer Service

Excellent customer service can enhance the investing experience, and both Schwab and Vanguard have built reputations for supporting their clients effectively. Schwab is known for its comprehensive customer support, offering 24/7 service through various channels, including phone, chat, and email. Their extensive network of physical branches also provides investors with personal assistance when needed.

Vanguard, while more digitally focused, offers robust customer service through online resources and phone support. They provide educational materials and tools to help investors make informed decisions, though some investors may miss the face-to-face interaction available at Schwab branches.

Online Platforms and Tools

In today's digital age, a user-friendly online platform is vital for managing investments efficiently. Schwab provides an intuitive platform with a wealth of tools and resources designed to help investors analyze and manage their portfolios. Their mobile app is highly rated, offering a seamless experience for investors on the go.

Vanguard's platform is similarly comprehensive, with a focus on simplicity and ease of use. Their online tools are designed to assist investors in planning and tracking their investments, though some users find the interface less modern compared to Schwab's offerings. Both companies continue to invest in technology to enhance the user experience and meet the evolving needs of their clients.

Social Responsibility and Ethics

As socially responsible investing gains traction, both Schwab and Vanguard have responded by offering funds that align with ethical and environmental values. Schwab's commitment to corporate responsibility is evident in their efforts to promote sustainable business practices and support community initiatives.

Vanguard has also embraced social responsibility, offering a range of ESG (Environmental, Social, and Governance) funds that cater to investors looking to make a positive impact through their investments. Both companies are recognized for their ethical business practices and dedication to meeting the needs of socially conscious investors.

Tax Efficiency

Tax efficiency is an important consideration for investors looking to maximize after-tax returns. Schwab and Vanguard both offer tax-efficient funds designed to minimize tax liabilities and enhance net returns. Schwab provides tax-managed funds that focus on reducing capital gains distributions and optimizing after-tax performance.

Vanguard's index funds are inherently tax-efficient due to their low turnover, meaning fewer capital gains are realized and distributed to investors. Vanguard also offers tax-managed funds aimed at high-net-worth investors seeking to minimize their tax exposure. Both companies provide tools and resources to help investors manage their tax obligations effectively.

Investment Minimums

Investment minimums can be a barrier for some investors, and both Schwab and Vanguard have taken steps to make their funds more accessible. Schwab generally has lower minimum investment requirements, making them an attractive option for new or smaller investors looking to enter the market.

Vanguard's minimums can be higher, especially for their Admiral Shares, which offer lower expense ratios for larger investments. However, Vanguard has lowered minimums for many of their funds, increasing accessibility for a broader range of investors. Both companies strive to balance affordability with the need to manage fund operations efficiently.

Reputation and Credibility

When evaluating Schwab index funds vs Vanguard, reputation and credibility are essential factors to consider. Schwab has built a strong reputation for innovation and customer service, earning the trust of millions of investors. Their focus on transparency and investor education further solidifies their standing in the industry.

Vanguard is renowned for its pioneering role in index investing and its investor-first approach. Their credibility is bolstered by their long track record of delivering consistent returns and maintaining low costs. Both companies are regarded as industry leaders, offering reliable investment options backed by years of expertise and experience.

Pros and Cons

When comparing Schwab index funds vs Vanguard, it's important to weigh the pros and cons of each provider. Schwab's strengths include a wide range of investment options, competitive fees, and excellent customer service. However, their selection of index funds may not be as extensive as Vanguard's, and some investors may prefer Vanguard's investor-owned structure.

Vanguard's advantages lie in their comprehensive range of low-cost index funds and their commitment to aligning their interests with investors. However, their customer service may not be as accessible as Schwab's, and their online platform may not appeal to all investors. Ultimately, the choice between Schwab and Vanguard will depend on individual investment goals and preferences.

FAQs

1. What are the main differences between Schwab index funds and Vanguard?

Schwab and Vanguard differ in their fund offerings, fee structures, and customer service models. Schwab offers a wide range of low-cost index funds with lower minimums, while Vanguard is known for its investor-owned structure and comprehensive selection of funds.

2. Which company offers lower fees for index funds?

Both Schwab and Vanguard are competitive in terms of fees, with Schwab often setting industry standards for low-cost investing. Vanguard's unique ownership structure allows them to maintain low fees as well.

3. Are Schwab index funds as tax-efficient as Vanguard's?

Both companies offer tax-efficient funds, with Schwab providing tax-managed options, and Vanguard's index funds benefiting from low turnover. Each provider offers resources to help investors optimize after-tax returns.

4. How do Schwab and Vanguard compare in terms of customer service?

Schwab is known for its excellent customer service, offering 24/7 support and a network of physical branches. Vanguard focuses on digital customer service and provides extensive online resources for investors.

5. Can new investors start with Schwab or Vanguard?

Yes, both Schwab and Vanguard cater to new investors. Schwab's lower minimums make it accessible for beginners, while Vanguard offers educational resources to help new investors understand their options.

6. Which company is better for socially responsible investing?

Both Schwab and Vanguard offer socially responsible investment options, with ESG funds available to align investments with ethical and environmental values.

Conclusion

Deciding between Schwab index funds vs Vanguard ultimately comes down to individual preferences and investment goals. Both companies offer compelling advantages, from Schwab's customer service and lower investment minimums to Vanguard's comprehensive fund offerings and investor-first approach. By carefully considering the factors outlined in this article, investors can make an informed choice that aligns with their financial objectives and personal values. As the landscape of index investing continues to evolve, Schwab and Vanguard remain at the forefront, providing investors with the tools and resources needed to achieve their investment aspirations.

For more detailed information about index fund investing, consider visiting the Investopedia guide to index funds.

You Might Also Like

Schwab Index Funds Vs Vanguard: A Comparative AnalysisHistorical Significance And Value Of The Barber Quarter 1907

Comprehensive Guide To Maximizing Returns With KIO Stock Dividend

Elon Musk's Signature Style: The Impact Of Sunglasses On His Image

Comprehensive Guide To Jasmy Order Book: Navigating The Digital Asset Landscape

Article Recommendations